DDP vs DAP: The Complete 2026 Guide for International Shipping (Updated & Compliant Version)

(Costs, Risks, VAT Recovery & Best Use Cases)

Expert Contributor: BSI Global Logistics Editorial Team |Last Updated: March 2026 | Industry Standards: Incoterms® 2020 Compliant

Introduction

When shipping goods internationally, choosing the right Incoterm directly affects your bottom line, legal risk, and customer satisfaction.

Among the 11 Incoterms®, DDP (Delivered Duty Paid) and DAP (Delivered at Place) are the most debated. While DDP offers a "hassle-free" experience, DAP provides "cost control." This guide breaks down the critical differences to help you choose the right strategy for your 2026 supply chain.

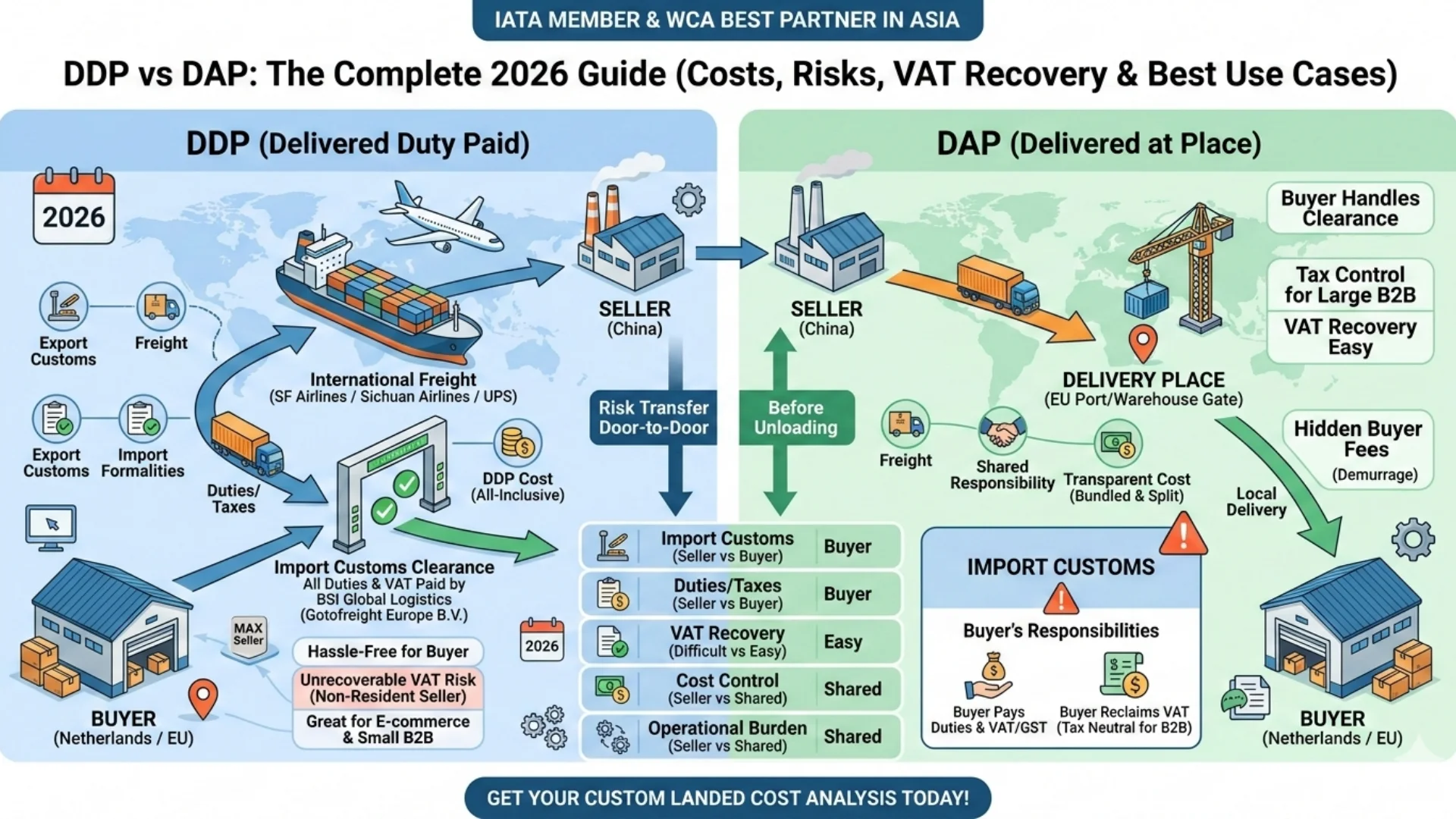

1. What Is DDP (Delivered Duty Paid)?

Under DDP, the seller assumes maximum responsibility and bears all risks until the goods reach the named destination specified by the buyer (e.g., the buyer’s warehouse door). It is important to clarify the unloading liability: under Incoterms 2020, DDP defaults to the seller not being responsible for unloading unless otherwise agreed in the contract. If the buyer requires the seller to handle unloading, the term "DDP Unloaded" must be clearly stated in the contract; otherwise, the buyer is obligated to unload the goods—a detail often overlooked by small and medium-sized B2B buyers, which may lead to performance disputes.

- Seller’s Scope: Export clearance, international freight,import customs clearance, and payment of all duties & VAT/GST.

- Buyer’s Scope: Unloading the goods upon arrival (unless "DDP Unloaded" is agreed).

💡 BSI Expert Insight: The "DDP Trap" in 2026

In the EU and UK, many sellers use DDP without being VAT registered in the destination country. This means the Import VAT paid at the border may become a permanent cost rather than a reclaimable tax—potentially eroding 20%–25% of your profit margin. However, it is not entirely impossible for non-resident sellers to reclaim VAT: they can do so through "Non-resident VAT Registration" with the help of a local tax agent, though the process is complex and requires additional agency fees (about 1%–2% of the goods value), which is still much lower than the cost of unrecoverable VAT. For example, a Chinese seller can normally reclaim 20% of import VAT in the UK by completing non-resident VAT registration through a local agent, with an agency cost of approximately $1,000–$2,000.

2. What Is DAP (Delivered at Place)?

Under DAP, the seller delivers the goods to the named destination and makes them ready for unloading, but the buyer handles the "legal" entry (customs clearance). It is crucial to note that the risk transfer point for DAP is "when the goods arrive at the named destination and are ready for unloading", which is irrelevant to whether customs clearance is completed. Customs clearance is the buyer’s responsibility, but risk transfer does not depend on the completion of customs clearance—even if the goods have arrived at the destination but not yet cleared customs, the risk has already transferred to the buyer (this is one of the core risk differences between DAP and DDP).

- Seller’s Scope: Transportation and risk until the goods are ready for unloading at the named place.

- Buyer’s Scope: Import customs clearance, payment of duties, and local taxes (VAT/GST). It should be noted that the buyer can only reclaim VAT smoothly if they are a VAT-registered entity in the destination country/region and the goods are used for "taxable business activities" (e.g., production, sales); if the buyer is an individual or a tax-exempt entity (such as some public welfare organizations), VAT cannot be reclaimed.

3. DDP vs DAP: Key Differences at a Glance

| Feature | DDP (Delivered Duty Paid) | DAP (Delivered at Place) |

| Import Clearance | Seller's Responsibility | Buyer's Responsibility |

| Duties & Taxes | Paid by Seller (VAT can be reclaimed via non-resident registration) | Paid by Buyer (VAT reclaimable if eligible) |

| Risk Transfer | At Named Destination (Before Unloading, unless "DDP Unloaded" is agreed) | At Named Destination (When Goods Are Ready for Unloading, irrelevant to customs clearance) |

| Best For | E-commerce / Small B2B / Samples | Large B2B / Experienced Importers / Tax-Sensitive Buyers |

| VAT Recovery | Possible but complex for non-resident sellers (requires local agent) | Easy for eligible local buyers (VAT-registered, taxable activities) |

4. Cost Structure & "Hidden" Fees

DDP: The "All-Inclusive" Price

The buyer sees one all-inclusive price. However, sellers often add a "buffer" to the DDP quote to cover potential customs delays, fluctuating tax rates, or additional costs such as non-resident VAT registration fees and local agent fees.

- Hidden Risk: If customs requires a physical inspection, the Storage & Exam fees are billed to the seller. In addition, if the seller fails to complete non-resident VAT registration, the import VAT paid will become an unrecoverable cost.

DAP: The "Transparent" Price

The buyer pays the freight to the seller but pays duties and taxes directly to the government. This model makes cost breakdown more transparent, and the buyer can reclaim VAT (if eligible) to reduce actual costs.

- Hidden Risk: If the buyer is slow to pay duties or lacks necessary customs clearance documents, the cargo gets stuck. Demurrage/Detention fees become the buyer's burden.

5. Critical Comparison: VAT Recovery & Tax Efficiency

This is the #1 reason why B2B transactions fail under DDP.

- Under DAP: The buyer is the Importer of Record (IOR). They pay the VAT and can usually reclaim it as an input tax credit (provided they are a VAT-registered entity and the goods are used for taxable activities). The tax is "neutral" and does not increase the buyer’s actual cost.

- Under DDP: If the seller (e.g., from China/USA) pays the VAT but does not have a local tax ID or complete non-resident VAT registration, that VAT is lost. For a $100,000 shipment to Poland, that is a $23,000 unrecoverable loss if no registration is done. Even with registration, the seller needs to bear agency fees, which still increases the overall cost.

Pro Tip: For high-value B2B cargo, DAP is often 20% more cost-effective for the buyer because of VAT recovery and no additional agent/qualification costs for the seller.

2026 DDP vs DAP Cost Comparison Case

Taking "100 industrial motors, value $100,000, HS Code 85016400" as an example, the cost breakdown in three core markets (EU/Poland, USA, India) is as follows, helping you intuitively compare the cost differences between the two terms:

| Incoterm | Total Cost in EU (Poland) | Total Cost in USA (California) | Total Cost in India | Key Differences |

| DDP (Non-resident Seller) | $100,000 (Goods Value) + $5,000 (Freight) + $12,000 (Duty, 12%) + $23,460 (VAT, 23%, unrecoverable without registration) + $1,500 (Customs Clearance Fee) + $2,000 (Non-resident VAT Registration Fee) = $143,960 | $100,000 + $6,000 (Freight) + $10,000 (Duty, 10%) + $8,800 (Sales Tax, 8.8%, unrecoverable for non-residents) + $2,000 (Customs Clearance Fee) = $126,800 (No VAT in USA, only sales tax) | $100,000 (Goods Value) + $8,000 (Freight) + $15,000 (Duty, 15%) + $26,450 (GST, 18%, unrecoverable) + $3,000 (Customs Clearance Fee) + $4,000 (IOR Qualification Fee) = $156,450 (IOR qualification required for DDP in India) | Taxes unrecoverable; additional agent/qualification costs; high total cost |

| DAP | $100,000 (Goods Value) + $5,000 (Freight) + $1,500 (Clearance Assistance Fee) = $106,500 (Buyer pays additional $12,000 duty + $23,460 VAT, fully reclaimable) | $100,000 + $6,000 (Freight) + $2,000 (Clearance Assistance Fee) = $108,000 (Buyer pays additional $10,000 duty + $8,800 sales tax, reclaimable for enterprises) | $100,000 + $8,000 (Freight) + $2,500 (Clearance Assistance Fee) = $110,500 (Buyer pays additional $15,000 duty + $26,450 GST, reclaimable; no IOR required for seller) | Taxes reclaimable; no additional qualification costs; lower actual cost for buyer Note: This case is calculated based on the latest 2026 tax rates and policies in core markets, including 18% GST in India, 23% VAT in the EU (Poland), and 8.8% sales tax in the USA (California). Actual costs may vary slightly depending on the goods' HS code and origin policies; it is recommended to verify with local customs for the latest regulations. |

6. Strategic Recommendations: Which One to Choose?

Choose DDP if:

- Cross-Border E-commerce: You are selling on Amazon, Shopify, or eBay. Customers expect a "local" experience with no surprise bills. (Note: If unloading is required, specify "DDP Unloaded" in the contract.)

- New Markets: Your buyer has zero experience with customs and wants a "Door-to-Door" service. For non-resident sellers, consider completing non-resident VAT registration to reclaim import VAT.

- Samples/Small Parcels: Low-value goods where the duty is minimal, and the cost of non-resident VAT registration outweighs the benefits of VAT recovery.

Choose DAP if:

- Large Scale B2B: Your buyer is a registered company with its own customs broker and can handle customs clearance independently.

- Tax Sensitivity: The buyer needs to reclaim VAT to maintain their margins (the buyer must be a VAT-registered entity and use the goods for taxable activities).

- Complex Products: The goods require specific import licenses (medical, telecom) that only a local buyer can provide. DAP avoids the seller’s risk of failing to obtain local licenses.

- High-Tariff or High-Value Goods: Reduces the seller's financial exposure to tax hikes and unrecoverable VAT costs.

7. FAQ: Common Questions in 2026

Q: Does DDP include unloading?

A: No. Under Incoterms 2020, the seller delivers the goods ready for unloading. The buyer is responsible for the actual labor/equipment to unload. If the buyer requires the seller to handle unloading, the term "DDP Unloaded" must be clearly stated in the contract; otherwise, the buyer bears the unloading liability.

Q: What happens if the goods are seized by customs under DDP?

A: The seller is responsible. Since the seller is the one clearing the goods, any compliance failure or "rejection" stays on the seller's record and account. To avoid this, sellers should entrust local customs brokers and ensure all documents (e.g., certificate of origin, HS code) are accurate.

Q: Can I do "DDP" but make the buyer pay VAT?

A: There is no official Incoterms term like "DDP VAT Unpaid"—this is an informal industry expression that may cause misunderstandings among customs and both parties (some customs may refuse clearance under this term). Instead, it is more appropriate to use DAP and add a specific contract clause stating that "the seller assists the buyer in completing customs clearance, while the buyer is responsible for paying VAT."

Q: What documents are required for DDP vs DAP shipments in 2026?

A: For DDP, sellers need to prepare full documents: commercial invoice, packing list, certificate of origin, export license (if applicable), and any destination-specific documents (e.g., EU EORI number, UK VAT registration certificate for non-resident sellers). For DAP, sellers provide basic shipping documents (invoice, packing list, bill of lading), while buyers prepare import clearance documents (local tax ID, import license, and any industry-specific certificates) since they handle customs entry. Note that in 2026, the EU and UK require electronic customs declarations for all DDP/DAP shipments, so digital document submission is mandatory.

Q: How does currency fluctuation affect DDP and DAP costs?

A: Currency fluctuation impacts both terms, but the risk falls on different parties. For DDP, the seller bears the risk—if the destination currency appreciates, the seller’s actual cost (duties, VAT, local fees) increases, as these are paid in the local currency. For DAP, the buyer bears the currency risk, as they pay duties and taxes in the local currency. To mitigate this, sellers can add a currency adjustment clause in DDP quotes, while buyers can lock in exchange rates when planning DAP payments.

Q: Can DAP or DDP be used for both sea and air freight in 2026?

A: Yes, both Incoterms are applicable to all modes of transport (sea, air, road, rail) under Incoterms 2020. However, there are minor differences in practice: for air freight (especially small parcels), DDP is more common for e-commerce or samples, as it simplifies the buyer’s experience. For sea freight (bulk cargo), DAP is preferred for large B2B transactions, as it allows the buyer to control customs clearance and VAT recovery. Note that for air freight DDP, sellers must ensure compliance with air cargo security regulations (e.g., EU ACAS) to avoid delays.

8. Final Decision Matrix

| Scenario | Recommended Term | Why? |

| Selling to Amazon FBA | DDP | Amazon will not act as the Importer of Record. Specify "DDP Unloaded" if Amazon requires unloading assistance. |

| Bulk Industrial Parts | DAP | Buyer needs the VAT receipt for tax deduction (assuming the buyer is a VAT-registered entity). |

| Air Freight Samples | DDP | Convenience outweighs the small tax cost; non-resident VAT registration is not cost-effective for low-value samples. |

| High Tariff Goods | DAP | Reduces the seller's financial exposure to tax hikes and unrecoverable VAT; buyer can reclaim taxes to control costs. |

| Shipments to India | DAP | DDP requires expensive IOR qualification; DAP avoids this cost and transfers customs clearance risk to the local buyer. |

9. Need a Custom Cost-Benefit Analysis?

Don't guess your margins. BSI Global Logistics provides Landed Cost Calculations for both DDP and DAP scenarios across Europe, India, and the Americas, tailored to your specific goods and destination.

Related Resources